Provider enrollment and credentialing is the two-step process that allows healthcare providers to bill insurance companies for their services. Credentialing verifies your qualifications and background, while enrollment adds you to insurance networks and assigns billing numbers. Together, they typically take 90-120 days and are mandatory for any provider who wants to accept insurance payments.

Table of Contents

- What Is Provider Enrollment?

- What Is Provider Credentialing?

- Provider Enrollment vs Credentialing: The Key Differences

- Why Provider Enrollment and Credentialing Matters

- Who Needs Provider Enrollment and Credentialing?

- The Step-by-Step Process

- Required Documents

- How Long Does It Take?

- Common Mistakes That Cause Delays

- Can You See Patients Before Enrollment Is Complete?

- Should You Outsource This Process?

- Specialty-Specific Considerations

- Frequently Asked Questions

What Is Provider Enrollment? (The Administrative Gateway to Getting Paid)

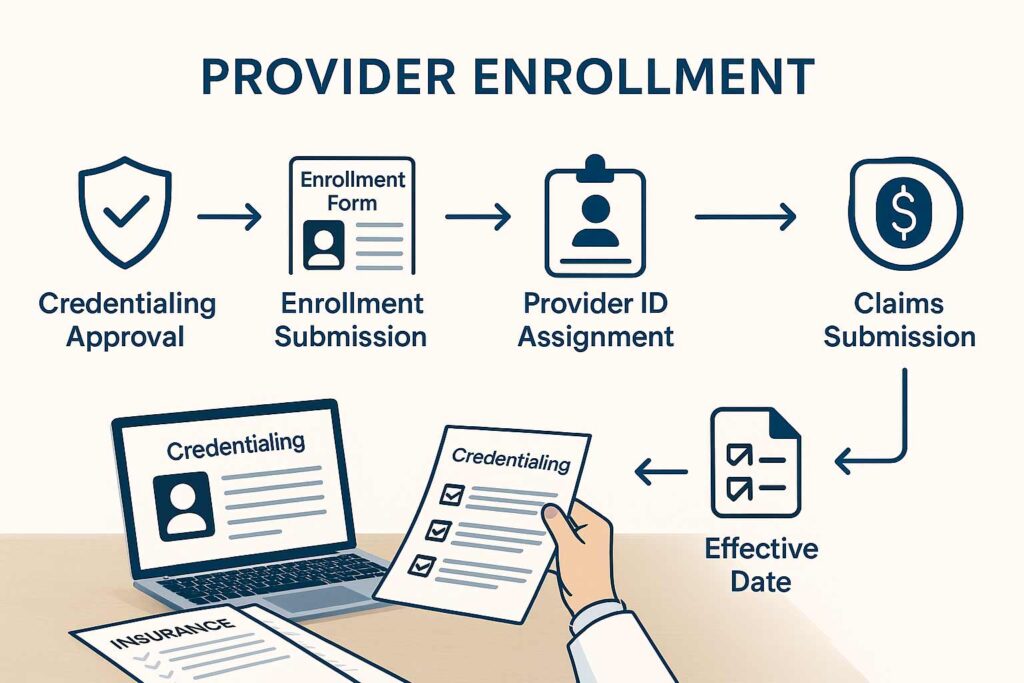

Provider enrollment is the administrative process where insurance companies officially add you to their networks and set you up in their billing systems. Think of it as getting your keys to the payment kingdom.

Here’s what actually happens during enrollment: After you’ve been credentialed (more on that in a second), the insurance company processes your participation paperwork, assigns you provider identification numbers, establishes your effective date, and configures their claims system to recognize and pay your claims.

Why Insurance Companies Require Enrollment

Insurance companies need enrollment to:

- Track provider participation across their networks

- Assign unique billing identifiers so claims route correctly

- Establish reimbursement rates based on your contract terms

- Set effective dates that determine when services become billable

- Configure claims processing in their payment systems

- Maintain network directories for member access

Without enrollment, you’re invisible to the insurance company’s billing infrastructure. Your claims get rejected with “provider not found” errors, even if you’re perfectly qualified.

How Enrollment Connects to Billing and Reimbursement

Enrollment is the final bridge between seeing patients and getting paid by insurance. Here’s the connection:

You see a patient → You submit a claim → The payer’s system checks if you’re enrolled → If yes, the claim processes for payment → If no, instant rejection.

Your enrollment also determines:

- Which services you’re authorized to bill

- Your reimbursement rates for each procedure code

- Whether you’re in-network or out-of-network

- Your tax identification and payment address

- Special billing requirements or modifiers

The cash flow reality: Even after enrollment completes, claims take 30-45 days to process and pay. So from enrollment completion to actual payment, you’re looking at another 1-2 months.

Insert image of provider enrollment workflow diagram here

What Is Provider Credentialing? (The Background Check That Never Ends)

Provider credentialing is the verification process where insurance companies investigate your qualifications, background, and professional history to determine if you meet their participation standards.

It’s basically the most thorough job application you’ll ever complete, except it happens with every single insurance company you want to work with.

What Insurance Companies Actually Verify

During credentialing, payers verify:

Educational Background

- Medical school or professional degree from accredited institutions

- Residency and fellowship training completion

- Board certification status (if applicable)

Professional Licensing

- Active state medical or professional licenses

- DEA registration for controlled substances

- State-specific certifications or permits

Professional History

- Complete work history for the past 10 years

- Explanation of any gaps in employment

- Hospital privileges and affiliations

- Academic appointments

Insurance and Liability

- Professional liability (malpractice) insurance with adequate limits

- Coverage for all procedures you perform

- Current and continuous coverage

Background and Sanctions

- National Practitioner Data Bank (NPDB) query

- Office of Inspector General (OIG) exclusion screening

- State medical board disciplinary actions

- Medicare/Medicaid sanctions history

- Criminal background checks

Professional References

- Verification with peer references

- Confirmation of professional standing

- Character and competency assessments

This isn’t a quick rubber-stamp process. Payers use primary source verification, meaning they contact your medical school, licensing boards, insurance carriers, and references directly rather than just trusting the documents you provide.

The Difference Between Credentialing and Licensing

People confuse these constantly, so let’s clear it up:

Licensing is issued by state governments and gives you legal authority to practice medicine or healthcare in that state. You get licensed once per state, and it’s a prerequisite for credentialing.

Credentialing is done by each insurance company individually and determines whether they’ll contract with you to provide services to their members. You need credentialing with every payer you want to bill.

You can be licensed but not credentialed (you can practice but can’t bill insurance). You cannot be credentialed without being licensed (payers require valid licenses).

Provider Enrollment vs Credentialing: What’s the Difference? (They’re Sequential, Not Synonymous)

The terms get used interchangeably, which creates massive confusion. They’re actually two distinct phases of the same overall process.

Here’s the side-by-side breakdown:

| Aspect | Provider Credentialing | Provider Enrollment |

| Purpose | Verify qualifications and background | Add provider to network and billing system |

| When It Happens | First step in the process | Happens after credentialing approval |

| What’s Being Done | Background verification, license checks, reference validation | Assignment of provider numbers, effective date establishment, system configuration |

| Who Performs It | Credentialing department at insurance company | Enrollment/provider relations department |

| Timeline | 60-120 days typically | 2-4 weeks after credentialing approval |

| What You Receive | Credentialing approval letter | Provider ID numbers, effective date, participation agreement |

| Can You Bill? | No, not yet | Yes, once enrollment completes |

How This Actually Plays Out in Real Life

Step 1: You submit credentialing applications to insurance companies

Step 2: Payers spend 60-120 days verifying your credentials (credentialing phase)

Step 3: You receive credentialing approval

Step 4: Payers process enrollment paperwork over 2-4 weeks

Step 5: You receive provider numbers and effective date

Step 6: You can now submit billable claims

The gap between credentialing approval and enrollment completion causes confusion and cash flow problems. You think you’re “approved” and ready to bill, but you’re actually still 2-4 weeks away from submitting your first claim.

Always ask: “Am I credentialed, enrolled, or both?” Don’t assume approval means you can bill.

Why Provider Enrollment and Credentialing Is Important (Beyond Just Getting Paid)

Obviously, enrollment and credentialing determine whether you get paid by insurance. But the implications run deeper than just revenue.

Getting Paid by Insurance Companies

This is the primary driver. Without enrollment and credentialing:

- You can’t submit claims to insurance

- Patients must pay out-of-pocket for all services

- Your patient base shrinks dramatically (most people need insurance coverage)

- Your practice revenue is severely limited

In most markets, 70-90% of patients require insurance participation from their providers. Operating cash-pay-only restricts you to a tiny market segment.

Legal and Compliance Requirements

Attempting to bill insurance without proper credentialing and enrollment isn’t just ineffective—it can be illegal.

Submitting claims under another provider’s credentials is fraud, even if that provider works in your practice.

Misrepresenting your network status to patients violates consumer protection laws.

Billing for services before your effective date violates payer contracts and can trigger investigations.

Healthcare compliance isn’t optional. Proper credentialing and enrollment keep you on the right side of regulations.

Patient Trust and Network Participation

Patients trust credentialed providers more. The credentialing process signals that:

- You’ve been vetted by major insurance companies

- Your qualifications have been verified

- You meet professional standards

- You’re part of established healthcare networks

Being in-network also dramatically affects patient access. Patients search insurance directories for providers, and if you’re not listed, you’re invisible to potential patients.

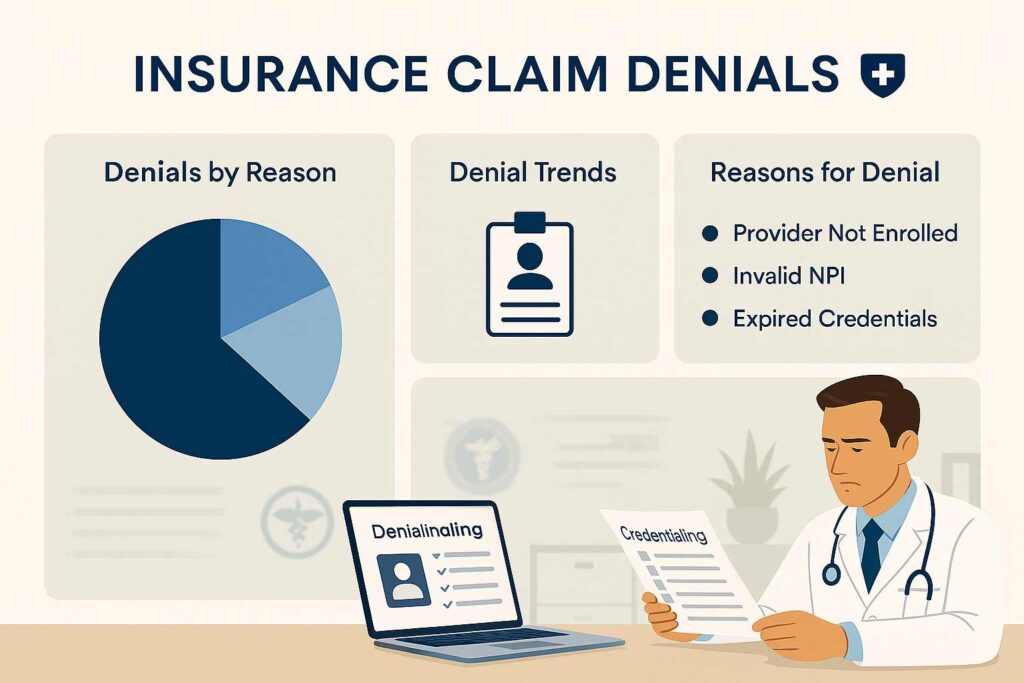

Avoiding Claim Denials

Even after you’re enrolled, maintaining current credentialing prevents claim denials. Common denial reasons related to credentialing:

- “Provider not found in system” (enrollment lapsed)

- “Services not covered for this provider” (credentialing doesn’t include all your services)

- “Provider contract terminated” (recredentialing deadline missed)

- “Invalid provider number” (credentialing information incorrect)

These denials delay payment by 60-90 days while you sort out the issues, creating cash flow nightmares.

Who Needs Provider Enrollment and Credentialing? (Pretty Much Everyone Who Bills Insurance)

If you’re providing healthcare services and want insurance to pay for them, you need enrollment and credentialing. Let’s break down who specifically needs this:

Individual Physicians and Providers

Every individual healthcare provider needs credentialing, including:

- Physicians (MD, DO)

- Nurse practitioners (NP)

- Physician assistants (PA)

- Clinical nurse specialists (CNS)

- Certified registered nurse anesthetists (CRNA)

- Physical therapists (PT)

- Occupational therapists (OT)

- Mental health professionals (psychologists, licensed clinical social workers, licensed professional counselors)

- Chiropractors (DC)

- Podiatrists (DPM)

Each provider credentials individually under their own NPI (National Provider Identifier), even if they work in a group practice.

Group Practices

Group practices need both:

- Individual credentialing for each provider

- Group credentialing for the practice entity itself

The group NPI allows centralized billing and administration, while individual NPIs enable provider-specific tracking and performance metrics.

Hospitals and Health Systems

Hospitals need:

- Facility credentialing for the organization

- Individual credentialing for employed physicians and advanced practice providers

- Privileging which is separate but related to credentialing

Hospital credentialing is more complex because it involves both insurance credentialing and internal privileging committees.

Labs, DME, Home Health, and Ambulatory Surgical Centers

Non-physician healthcare entities require credentialing too:

Durable Medical Equipment (DME) suppliers need Medicare supplier enrollment and commercial payer credentialing to bill for equipment.

Home health agencies need facility enrollment with Medicare, Medicaid, and commercial payers, plus individual credentialing for nurses and therapists.

Ambulatory Surgical Centers (ASCs) need facility credentialing separate from the surgeons who perform procedures there.

Pathology labs need CLIA certification, facility credentialing, and individual credentialing for pathologists.

Telehealth Providers

Telehealth adds complexity because you need:

- Credentialing in every state where you see patients

- State-specific licenses for each state

- Payer-specific telehealth participation agreements

- Compliance with varying state telemedicine laws

A telehealth psychiatrist seeing patients across 10 states needs credentialing with payers in all 10 states, which multiplies the administrative burden significantly.

Step-by-Step Provider Enrollment and Credentialing Process (From Start to First Payment)

Here’s exactly how the process unfolds from day one through your first insurance payment:

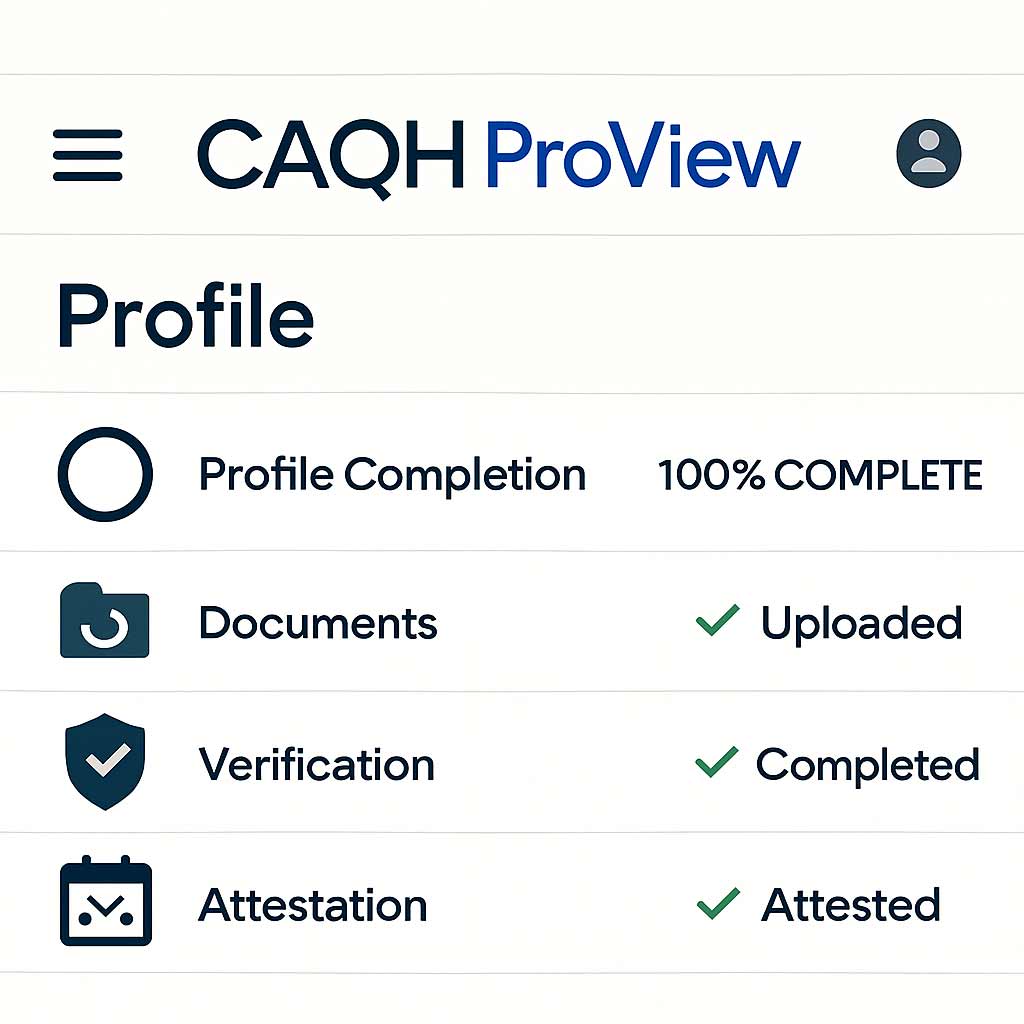

Step 1: NPI and CAQH Setup

What happens: You obtain your National Provider Identifier (NPI) from NPPES and create your CAQH ProView profile.

Timeline: 1-2 weeks

Critical actions:

- Apply for NPI at nppes.cms.hhs.gov (free, instant approval for most)

- Register at caqh.org using your NPI

- Complete every section of your CAQH profile

- Upload all supporting documents

- Attest your profile (this step is critical—payers can’t access unattested profiles)

Common mistakes: Leaving sections blank, uploading expired documents, forgetting to attest

Step 2: Document Collection

What happens: You gather every document required for credentialing applications.

Timeline: 1-2 weeks (if you’re organized; 4-6 weeks if you’re not)

Required documents:

- Medical degree and training certificates

- State licenses (all states where you practice)

- Board certifications

- DEA and controlled substance registrations

- Malpractice insurance certificates

- Professional references contact information

- Complete work history documentation

- NPDB self-query report

Pro tip: Create a master credentialing folder with digital copies of everything. You’ll submit the same documents repeatedly to different payers.

Step 3: Payer Application Submission

What happens: You submit credentialing applications to each insurance company you want to work with.

Timeline: 1-2 weeks for submission prep

Key decisions:

- Which payers to apply to (prioritize based on patient demographics)

- Individual vs group credentialing approach

- Which locations to include in applications

Application methods:

- Some payers use CAQH exclusively

- Others require payer-specific applications in addition to CAQH

- Medicare uses PECOS (Provider Enrollment, Chain and Ownership System)

- Medicaid varies by state

Step 4: Primary Source Verification

What happens: Insurance companies verify everything you submitted by contacting original sources directly.

Timeline: 60-90 days (this is the longest phase)

What payers are doing:

- Contacting your medical school to verify your degree

- Checking with state medical boards for license verification

- Calling your malpractice insurance carrier

- Reaching out to your professional references

- Querying NPDB for malpractice history

- Running OIG exclusion screening

Why it takes so long: Payers are waiting on responses from third parties who aren’t particularly motivated to respond quickly.

Step 5: Credentialing Approval and Effective Date

What happens: You receive credentialing approval and your participation effective date.

Timeline: Immediate once verification completes

What you receive:

- Credentialing approval letter

- Effective date (the date from which your services are billable)

- Next steps for enrollment completion

Critical detail: Your effective date might be your application date, approval date, or a future date—this varies by payer and dramatically affects which services you can bill for.

Step 6: Enrollment Confirmation and Provider Numbers

What happens: The payer processes your enrollment and assigns billing identifiers.

Timeline: 2-4 weeks after credentialing approval

What you receive:

- Provider ID numbers for claims submission

- Payer-specific billing guidelines

- Participation agreement terms

- Reimbursement fee schedules

- Network directory listing confirmation

Final step: Configure your billing system with correct provider numbers and payer IDs, then submit your first claims.

Documents Required for Provider Enrollment and Credentialing (The Complete Checklist)

Missing even one document triggers rejections and restarts the timeline. Here’s everything you need:

Provider Credentials and Education

- Medical degree (MD, DO, or other professional degree)

- Residency completion certificate

- Fellowship certificates (if applicable)

- Board certification from recognized specialty boards

- CME (Continuing Medical Education) certificates

- Specialty training documentation

Professional Licensing

- State medical license (current and active for every state where you practice)

- DEA registration certificate (if prescribing controlled substances)

- State controlled substance licenses

- CLIA certificate (if operating a lab)

- Any specialty-specific licenses or permits

National Provider Identifier (NPI)

- Type 1 NPI (individual provider)

- Type 2 NPI (organizational/group, if applicable)

- NPI validation printout from NPPES

Practice Information

- Legal practice name and DBA (doing business as) if different

- Tax ID (EIN) for the practice

- Practice physical address (no P.O. boxes accepted)

- Phone, fax, email contact information

- Office hours and patient capacity

- Ownership structure and percentages

Insurance and Liability Coverage

- Professional liability insurance (malpractice) certificate

- Minimum coverage typically $1M per occurrence / $3M aggregate

- Current policy dates (must be continuous, no lapses)

- Tail coverage documentation if switching carriers

- General liability insurance for the practice

Work History and References

- Complete employment history for past 10 years

- Dates, locations, and positions for each role

- Explanation letters for any employment gaps over 30 days

- Three professional references (typically physician colleagues)

- Reference contact information (phone and email)

- Hospital privileges documentation (if applicable)

Background and Compliance Verification

- NPDB (National Practitioner Data Bank) self-query report

- State medical board verification letter

- OIG (Office of Inspector General) exclusion screening

- SAM (System for Award Management) screening

- Disclosure of any malpractice claims or settlements

- Disclosure of any disciplinary actions or investigations

Banking and Tax Information

- W-9 form for tax reporting

- Direct deposit enrollment form (ACH information)

- Practice bank account details

- Taxpayer identification verification

CAQH-Specific Requirements

- Professional headshot (business appropriate, recent)

- Signed attestation (updated every 120 days)

- Digital copies of all credentials in acceptable formats (usually PDF)

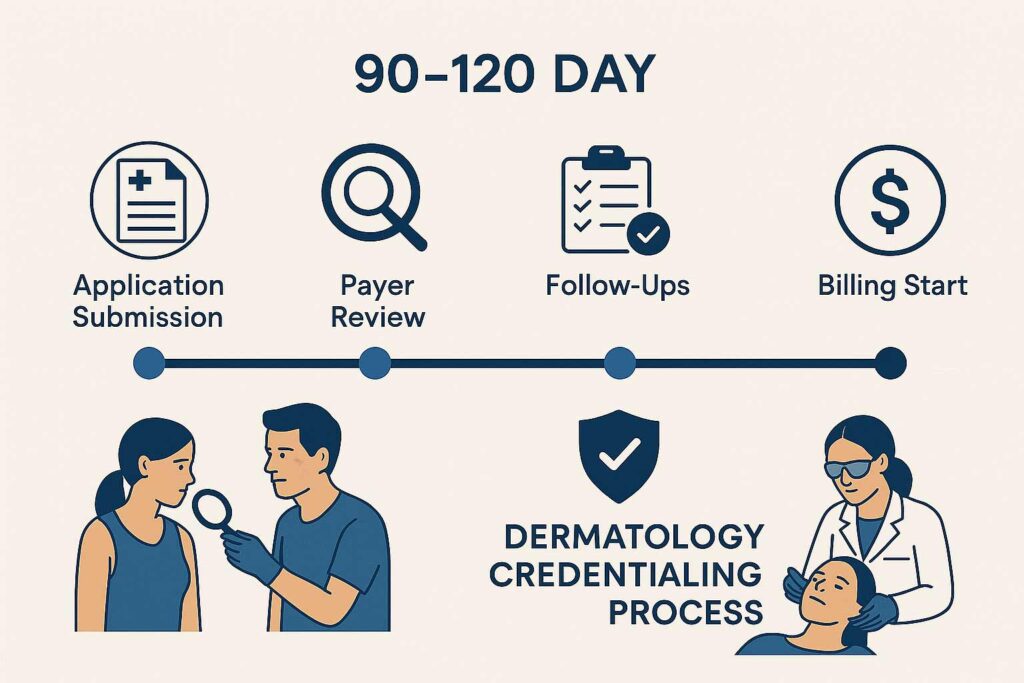

How Long Does Provider Enrollment and Credentialing Take? (The Realistic Timeline)

Everyone wants a simple answer to “how long does this take?” Unfortunately, timelines vary significantly based on payer type, practice structure, and how organized you are.

Medicare Enrollment Timeline

Average: 60-90 days

Medicare enrollment through PECOS is usually faster than commercial payers because it’s a standardized federal process.

Factors that speed it up:

- Complete, error-free applications

- All documents current and valid

- No ownership complexity

- Single practice location

Factors that slow it down:

- Incomplete applications (restart the clock)

- Ownership structure verification delays

- Multiple locations requiring individual enrollment

- Background issues requiring additional review

Medicaid Enrollment Timeline

Average: 90-120 days

Medicaid timelines vary dramatically by state because each state administers its own program.

Fastest states (60-90 days):

- Texas

- Illinois

- Georgia

- Florida (when not backlogged)

Slower states (90-150 days):

- California

- New York

- Michigan (high scrutiny states)

State-specific quirks: Some states require site visits, additional background checks, or provider interviews that add weeks to the process.

Commercial Insurance Credentialing Timeline

Average: 90-120 days

Commercial payers (BCBS, Aetna, Cigna, UnitedHealthcare, Humana) have similar timelines, though individual experiences vary.

| Payer | Typical Timeline | Notes |

| Blue Cross Blue Shield | 90-120 days | Varies by state plan |

| UnitedHealthcare | 90-120 days | Strict verification standards |

| Aetna | 90-120 days | Fast-track available in some markets |

| Cigna | 90-120 days | Generally consistent |

| Humana | 90-120 days | Medicare Advantage can be faster |

| Regional plans | 60-150 days | Highly variable |

Timeline factors:

- First-time applicants take longer than re-credentialing

- Group practices require additional verification

- Multi-location practices add 2-4 weeks per site

- Specialty-specific requirements extend timelines

New vs Established Practices

New practices: Plan for 4-6 months from credentialing start to first payment received

Established practices adding providers: 3-4 months typically

Practices adding locations: 2-3 months (faster because practice infrastructure exists)

The Real-World Timeline

Here’s what the complete process looks like from day one:

Month 1: NPI setup, CAQH profile creation, document gathering

Month 2: Application submissions to top payers

Month 3: Verification process ongoing, follow-ups begin

Month 4: First approvals arrive (typically smaller/regional payers)

Month 5: Major commercial payers complete enrollment

Month 6: Submit first claims, receive first payments

That’s six months from starting credentialing to cash in the bank. This is why new practices need significant operating capital.

Common Provider Enrollment and Credentialing Mistakes (That Add Months to Your Timeline)

I’ve seen providers make the same mistakes repeatedly, and each one costs weeks of delays. Here are the top offenders:

Mistake #1: Incomplete or Unattested CAQH Profiles

The problem: You complete 95% of your CAQH profile but leave one section blank, or you forget to click “attest” at the end.

The consequence: Payers can’t access your information. Your application sits in limbo while you think it’s being processed.

The fix: Complete every single field. If something doesn’t apply, mark it “N/A” rather than leaving it blank. Set a calendar reminder to attest every 120 days.

Time lost: 2-6 weeks typically

Mistake #2: Expired or Expiring Documents

The problem: Your malpractice insurance or state license expires during the credentialing process.

The consequence: Payers reject your application or halt processing until you provide updated documents.

The fix: Ensure all documents are valid for at least 6 months beyond your application date. Update CAQH immediately when credentials renew.

Time lost: 2-4 weeks per expired document

Mistake #3: Address Inconsistencies Across Documents

The problem: Your practice address on your medical license shows Suite 100, your CAQH profile shows Suite 101, and your payer application shows Unit 100.

The consequence: Payers flag this as a verification failure and require clarification.

The fix: Use exactly the same address format across all documents—same abbreviations, same suite numbers, identical formatting.

Time lost: 1-3 weeks

Mistake #4: Unresponsive or Wrong Professional References

The problem: You list references who don’t respond to payer inquiries, or you list colleagues who don’t actually know your work well enough to provide meaningful references.

The consequence: Credentialing stalls while payers attempt to reach references multiple times.

The fix: Choose references who respond quickly to emails and calls. Give them a heads-up that they’ll be contacted. Confirm their current contact information. Choose colleagues who can speak to your clinical competence and professional character.

Time lost: 2-4 weeks

Mistake #5: Waiting Passively Instead of Following Up

The problem: You submit applications and assume payers will contact you if they need anything.

The consequence: Applications sit in queues, missing information goes unrequested, and timelines stretch indefinitely.

The fix: Follow up with every payer every 7-10 days. Call credentialing departments directly. Ask for specific status updates and timeline estimates. Be proactive about providing additional information.

Time lost: 4-12 weeks (this is the biggest time waster)

Mistake #6: Applying to Too Many Payers Simultaneously

The problem: You submit applications to 20+ insurance companies at once, thinking more is better.

The consequence: You can’t effectively follow up on all applications, responses get missed, and you’re overwhelmed managing the process.

The fix: Start with 5-7 top payers based on your patient demographics. Once those are complete, add more. Quality over quantity.

Time lost: Variable, but managing too many applications simultaneously often extends all timelines

Mistake #7: Missing State-Specific Medicaid Requirements

The problem: Each state has unique Medicaid credentialing requirements you didn’t research.

The consequence: Applications get rejected for missing state-specific forms, background checks, or compliance documentation.

The fix: Research state Medicaid requirements thoroughly before applying, or work with credentialing services that know state-specific rules.

Time lost: 4-8 weeks

Mistake #8: Not Understanding Group vs Individual Credentialing

The problem: You apply for individual credentialing when you should apply for group, or vice versa.

The consequence: Applications get rejected or processed incorrectly, requiring resubmission.

The fix: Clarify your practice structure with payers before applying. Understand whether you need individual, group, or both types of credentialing.

Time lost: 4-8 weeks (essentially starting over)

Can Providers See Patients Before Enrollment Is Complete? (Yes, But Here’s What You Need to Know)

You can absolutely see patients before credentialing and enrollment finish, but there are strict limitations on what you can—and cannot—do.

What You Can Legally Do

Accept cash-pay patients: You can see patients who pay out-of-pocket for services at the time of visit. Set your own rates and collect payment directly.

Provide services at discounted self-pay rates: Many providers offer 30-50% discounts off standard rates for patients paying cash during the credentialing period.

Generate superbills for patients: Create detailed receipts showing CPT codes, diagnosis codes, and charges that patients can submit to their insurance for potential out-of-network reimbursement.

See patients who don’t have insurance: Uninsured patients can access your services regardless of your credentialing status.

Offer payment plans: You can establish payment arrangements with patients for services rendered before credentialing completes.

What You Absolutely Cannot Do

Submit claims to insurance companies: Without enrollment, your claims will be rejected immediately with “provider not found” errors.

Tell patients their insurance will cover services: This is misrepresentation. You must inform patients that you’re not yet credentialed and their insurance won’t pay.

Use another provider’s credentials: Billing under a colleague’s NPI while you’re waiting for credentialing is fraud, even if they work in your practice.

Promise retroactive billing without confirmation: Some payers allow retroactive billing after credentialing, but most don’t. Never promise this unless you’ve confirmed the payer’s specific policy.

Accept insurance assignment: You can’t legally accept insurance as payment without being credentialed and enrolled with that specific payer.

The Financial Reality of Seeing Patients Pre-Credentialing

Most practices can’t survive long-term on cash-pay alone. Here’s why:

Patient volume drops 60-80%: Most patients require insurance participation. When you tell them “we don’t take insurance yet,” many go elsewhere.

Revenue per visit is lower: Even with self-pay rates, you’re typically collecting less than insurance reimbursement, and collection rates aren’t 100%.

Administrative burden increases: Managing cash collections, payment plans, and superbills adds workload.

Cash flow remains tight: You need immediate payment to cover operating expenses, which limits your patient base to those who can pay upfront.

Strategies to Manage the Pre-Credentialing Period

- Be transparent with patients: Clearly communicate your credentialing status and payment options from the initial appointment call.

- Offer attractive self-pay rates: Consider 30-40% discounts to make cash payment more palatable.

- Focus on services with higher cash-pay demand: Certain specialties (dermatology aesthetics, mental health, physical therapy) have more cash-pay patient acceptance.

- Build your patient schedule: See patients during credentialing to establish relationships. Once enrolled, they’ll return for ongoing care covered by insurance.

- Investigate retroactive billing options: Some payers allow billing back to your application date—document every service carefully in case retroactive billing is approved.

Should You Outsource Provider Enrollment and Credentialing? (The Honest Cost-Benefit Analysis)

You can handle credentialing yourself, but the question is whether you should. Let’s break down the decision.

When DIY Credentialing Makes Sense

Consider handling it yourself if:

- You’re a solo provider credentialing with 3-5 payers only

- You have administrative staff with credentialing experience

- You have 20-30 hours to invest over 3-4 months

- You’re extremely detail-oriented and organized

- You don’t have time-sensitive revenue deadlines

- You’re credentialing in a single state only

When Outsourcing Makes More Sense

Outsource if:

- You’re opening a new practice and need revenue ASAP

- You’re adding multiple providers simultaneously

- You’re credentialing across multiple states

- You’re credentialing with 10+ payers

- You don’t have experienced administrative staff

- You can’t afford 4-6 month delays

- You’re operating a group practice or multi-location organization

- You want to focus on patient care, not paperwork

The Real Cost of DIY Credentialing

People think they’re saving money by handling credentialing themselves. Let’s look at the actual costs:

Your time investment:

- Initial setup: 10-15 hours

- Application completion: 2-3 hours per payer × 10 payers = 20-30 hours

- Follow-ups and status checks: 1 hour per week × 16 weeks = 16 hours

- Responding to requests for additional information: 5-10 hours

- Total: 51-71 hours minimum

Time value calculation: If your time is worth $150-300/hour as a provider (conservative estimate), you’re investing $7,650-21,300 in opportunity cost by handling it yourself.

Delay costs: Without expertise, your credentialing likely takes 30-60 days longer. Each week of delay costs you $5,000-15,000 in lost revenue depending on your specialty and patient volume.

What Professional Credentialing Services Provide

Complete application management: They handle every payer from start to finish.

CAQH optimization: They know exactly what payers look for and structure your profile for fastest approval.

Direct payer relationships: Established credentialing services have direct contacts at insurance companies who can expedite issues.

Proactive follow-up: They call payers weekly on your behalf, eliminating the endless hold times and voicemail tag.

Error prevention: They catch common mistakes before submission, preventing rejections.

Timeline acceleration: Professional services typically complete credentialing 30-45 days faster than DIY attempts.

Recredentialing management: They track revalidation deadlines and handle ongoing compliance.

Multi-state expertise: They know state-specific requirements that DIY providers miss.

The Cost of Professional Services

Typical pricing models:

- Per provider, per payer: $100-300 per application

- Comprehensive packages: $2,000-5,000 for 10-15 payers

- Ongoing management: $150-300/month for recredentialing and compliance monitoring

- Enterprise pricing: Custom pricing for large groups or health systems

The ROI Calculation

Investment: $3,000 for comprehensive credentialing services

Time saved: 50+ hours of your time = $7,500-15,000 value

Delay reduction: 30-45 days faster enrollment = $20,000-60,000 additional revenue

Error prevention: Avoiding a single rejected application = 4-8 weeks saved

Total value: $27,500-75,000+ for a $3,000 investment

The math is clear: for most providers, outsourcing credentialing delivers 10-25x ROI.

TrueCare RCM’s Provider Enrollment and Credentialing Services

TrueCare RCM specializes in provider enrollment and credentialing across all specialties and all 50 states. We handle:

- Complete CAQH profile setup and maintenance

- Medicare PECOS and Medicaid enrollment

- Commercial payer credentialing (all major insurance companies)

- Multi-state and multi-location credentialing

- Group and individual provider credentialing

- Recredentialing and compliance monitoring

- Integration with medical billing services

Our process:

- Free consultation and timeline assessment

- Document collection and organization

- Application submission to all targeted payers

- Weekly follow-ups and status tracking

- Issue resolution and expedited processing

- Final enrollment confirmation and billing setup

Provider Enrollment and Credentialing for Medical Specialties (Specialty-Specific Considerations)

Different medical specialties face unique credentialing challenges. Here’s what you need to know for major specialty categories:

Primary Care (Family Practice, Internal Medicine, Pediatrics)

Credentialing considerations:

- Broadest patient demographics require credentialing with 12-15 payers minimum

- Medicaid is critical for pediatrics

- Medicare is essential for internal medicine and family practice

- Fastest credentialing timelines (90-100 days typically)

Common issues: Managing high payer volume, ensuring pediatric-specific Medicaid enrollment

Surgical Specialties (Orthopedics, General Surgery)

Credentialing considerations:

- Facility credentialing often required in addition to individual credentialing

- Hospital privileges verification

Continue

5:16 AM

adds time

- Higher malpractice insurance requirements

- Procedure-specific documentation needed

Common issues: Coordinating facility and individual credentialing timelines, verifying surgical privileges

Behavioral Health and Mental Health

Credentialing considerations:

- State Medicaid is crucial (Medicaid covers significant behavioral health services)

- Telehealth credentialing increasingly important

- Some payers have separate behavioral health divisions

- Licensure varies significantly by provider type (psychologist, LCSW, LPC, psychiatrist)

Common issues: Multi-state telehealth credentialing, varying requirements by provider license type

Anesthesiology

Credentialing considerations:

- Often linked to facility or surgical center credentialing

- Hospital-based vs independent practice affects approach

- Medicare and commercial payers scrutinize heavily

- CRNA credentialing differs from physician anesthesiologist credentialing

Common issues: Coordinating with facilities, managing complex billing arrangements

Emergency Medicine

Credentialing considerations:

- Hospital employment often handles credentialing

- Independent EM groups need multi-facility credentialing

- Out-of-network arrangements more common

- Fast-track credentialing sometimes available

Common issues: Managing credentialing across multiple hospital contracts

Physical Therapy, Occupational Therapy

Credentialing considerations:

- Group practice credentialing common

- Multi-location practices standard

- Medicare therapy caps and documentation requirements

- Some states require additional facility licensing

Common issues: Managing credentialing for multiple locations simultaneously

Dermatology

Credentialing considerations:

- Medical vs cosmetic procedure delineation

- Mohs surgery requires additional documentation

- Dermatopathology needs lab credentialing

- Telehealth dermatology growing rapidly

Common issues: Clearly defining scope of practice, managing cosmetic vs medical billing

For detailed dermatology credentialing information, see our comprehensive guide on dermatology credentialing services.

DME, Home Health, and Ancillary Services

Credentialing considerations:

- Facility credentialing in addition to individual provider credentialing

- Medicare supplier enrollment critical

- Accreditation requirements (JCAHO, ACHC)

- State-specific facility licensing

Common issues: Coordinating facility and provider credentialing, meeting accreditation timelines

Frequently Asked Questions About Provider Enrollment and Credentialing

What is provider enrollment and credentialing in healthcare?

Provider enrollment and credentialing is the two-part process that allows healthcare providers to bill insurance companies. Credentialing verifies your professional qualifications, education, licenses, and background through primary source verification. Enrollment adds you to insurance networks and assigns provider identification numbers so you can submit claims. Together, these processes typically take 90-120 days and are required by every insurance company before they’ll pay for your services. Without completion of both credentialing and enrollment, claims are rejected as “provider not found.”

Is provider enrollment the same as credentialing?

No, they’re sequential but distinct processes. Credentialing comes first—it’s the verification of your qualifications and background. This includes checking your medical education, licenses, board certifications, malpractice insurance, and professional history. Enrollment happens after credentialing approval—it’s when the insurance company officially adds you to their network, assigns you provider billing numbers, and establishes your effective date. You must complete credentialing before enrollment can begin. Think of credentialing as getting approved and enrollment as getting your access keys to actually bill.

How long does provider enrollment and credentialing take?

Typical timelines are 90-120 days from application submission to final enrollment, but this varies significantly. Medicare PECOS enrollment averages 60-90 days. Medicaid varies by state from 60-150 days. Commercial payers (BCBS, UnitedHealthcare, Aetna, Cigna) typically take 90-120 days. New practices often experience longer timelines (120-150 days) due to additional verification requirements. Add another 30-45 days for claims processing after enrollment, meaning 4-6 months from starting credentialing to receiving your first insurance payment. Incomplete applications, expired documents, or unresponsive references can extend timelines significantly.

Can providers bill insurance before enrollment is complete?

No. Without completed credentialing and enrollment, you cannot submit billable claims to insurance companies. Claims submitted before enrollment are rejected immediately with “provider not found” or similar denial codes. You can see patients before credentialing completes, but you must collect payment directly from them—either cash-pay, discounted self-pay rates, or providing superbills for patients to submit for out-of-network reimbursement. Some payers allow retroactive billing back to your application date after enrollment completes, but this varies by payer. Never promise insurance coverage to patients until your enrollment is confirmed complete.

What documents are required for provider enrollment and credentialing?

Required documents include: medical degree and training certificates; all state medical licenses; board certification; DEA and controlled substance licenses; professional liability insurance (typically $1M/$3M minimum); NPI (National Provider Identifier); practice tax ID (EIN); complete work history for 10 years; three professional references; NPDB self-query report; practice address and contact information; W-9 form; banking information for direct deposit. You’ll also need a completed, attested CAQH profile. Specialty-specific requirements may include fellowship certificates, hospital privileges, facility licenses (for ASCs, labs, home health), or CLIA certification. All documents must be current and valid throughout the credentialing process.

What is CAQH and why is it required for credentialing?

CAQH ProView is a universal credentialing database used by over 1,400 insurance companies. Instead of completing separate applications for each payer, you create one comprehensive CAQH profile containing all your credentials, which participating insurance companies then access for verification. CAQH is free for providers and mandatory for credentialing with virtually all commercial payers. You must complete every section, upload supporting documents, and “attest” your profile (confirm accuracy) for payers to access your information. Re-attestation is required every 120 days to keep your profile active. Without a complete, attested CAQH profile, commercial insurance credentialing cannot proceed.

How often do providers need to recredential with insurance companies?

Most insurance companies require recredentialing every 2-3 years to verify your credentials remain current. Medicare requires revalidation through PECOS every 5 years. Your CAQH profile requires re-attestation every 120 days (quarterly), though this isn’t full recredentialing—just confirmation your information is accurate. State licenses typically renew every 1-2 years, board certifications every 10 years, and malpractice insurance annually—all triggering CAQH updates. Professional credentialing services track all renewal dates and initiate recredentialing 3-6 months before deadlines to prevent lapses that would result in network termination and claim denials.

What happens if credentialing expires or lapses?

Expired or lapsed credentialing results in network termination, meaning you can no longer bill that insurance company. All claims submitted after your termination date are denied. Patients may receive unexpected bills if they saw you assuming insurance coverage. Your practice loses revenue immediately—potentially tens of thousands per month depending on patient volume. Re-credentialing after a lapse is treated as new enrollment, requiring the full 90-120 day process. Some payers impose waiting periods before accepting applications from previously terminated providers. Prevention is critical: track all recredentialing deadlines and initiate renewal 3-6 months early. Professional credentialing services provide ongoing monitoring to prevent lapses.

Does each practice location need separate enrollment?

Yes, typically each physical location where you see patients requires separate enrollment with most insurance companies. When adding a new office, you must submit location-specific information and sometimes undergo site inspections. The credentialing process for new locations is usually faster (30-60 days) than initial credentialing since your provider credentials are already verified, but you cannot bill for services at the new location until that site-specific enrollment completes. Group practices can sometimes centralize billing under one location, but you must still register all service addresses with payers. Multi-state practices face additional complexity, requiring separate state licenses and state-specific payer credentialing.

What is the difference between individual and group credentialing?

Individual credentialing credentials each provider separately under their personal NPI (Type 1). The provider maintains their own contracts and billing relationships with payers. Group credentialing credentials the practice organization under a group NPI (Type 2), with individual providers listed as members of the group. Benefits of group credentialing include centralized billing, consistent contract terms across providers, and simplified administration. Many practices use both—group credentialing for organizational purposes while individual providers maintain their own credentialing for flexibility. Solo practitioners use individual credentialing only. Large groups typically require both individual and group credentialing depending on payer requirements.

How does Medicare enrollment differ from commercial insurance credentialing?

Medicare enrollment occurs through PECOS (Provider Enrollment, Chain and Ownership System), a federal online portal, rather than through CAQH. The process is more standardized nationwide compared to commercial payers. Medicare requires ownership disclosure, detailed practice location information, and stringent background screening. Medicare typically doesn’t accept “retroactive” enrollment—your effective date is when CMS approves your application. Medicare revalidation occurs every 5 years vs 2-3 years for commercial payers. Medicare Advantage plans (Part C) require separate credentialing with each commercial carrier (UnitedHealthcare, Humana, etc.) in addition to traditional Medicare PECOS enrollment, effectively doubling your Medicare credentialing workload.

Can enrollment be done for multiple states?

Yes, but each state requires separate licensing, and many payers require state-specific credentialing. If you practice in multiple states, you need a valid medical license in each state where you see patients (including telehealth patients located in that state). Medicaid requires separate enrollment in each state since it’s state-administered. Some commercial payers have regional divisions requiring state-specific applications (like Blue Cross Blue Shield state plans). The Interstate Medical Licensure Compact (IMLC) can expedite multi-state licensing for eligible physicians. Multi-state credentialing significantly increases timeline and administrative burden—expect to add 60-90 days per additional state for full payer panel credentialing.

What causes delays in provider enrollment and credentialing?

Common delay causes include: incomplete or unattested CAQH profiles (2-6 week delay); expired documents like licenses or malpractice insurance (2-4 weeks); address inconsistencies across documents (1-3 weeks); unresponsive professional references (2-4 weeks); missing specialty-specific documentation (2-4 weeks); payer backlogs during peak periods like January and July (4-12 weeks); state-specific Medicaid requirements you didn’t anticipate (4-8 weeks); failure to follow up regularly with payers (4-12 weeks). The single biggest delay factor is passive waiting instead of proactive follow-up. Calling payers weekly to check status and provide missing information can reduce timelines by 30-60 days.

Is outsourcing provider enrollment worth it?

For most providers, yes. Professional credentialing services typically cost $2,000-5,000 for comprehensive enrollment with 10-15 payers but deliver significant ROI through time savings (50+ hours of your time valued at $7,500-15,000), timeline acceleration (30-45 days faster = $20,000-60,000 additional revenue), and error prevention (avoiding rejections that cost 4-8 weeks). Outsourcing makes most sense for new practices needing fast revenue, multi-provider groups, multi-state practices, or providers credentialing with 10+ payers. DIY might work for solo providers with 3-5 payers, experienced administrative staff, and no time-sensitive deadlines. The cost-benefit analysis typically favors outsourcing 10-25x ROI for most scenarios.

How does enrollment affect medical billing and cash flow?

Enrollment directly determines when you can generate insurance revenue. Without completed enrollment, all claims are rejected, creating a 90-120 day cash flow gap during credentialing. Add 30-45 days for claims processing after enrollment, and new practices need 6-8 months of operating capital from credentialing start to first payment. Each week of enrollment delay costs $5,000-15,000+ in lost revenue for typical practices. Even after enrollment completes, claim denials due to credentialing errors (wrong provider numbers, services not authorized, expired credentials) disrupt cash flow for 60-90 days while being resolved. Professional billing services integrate credentialing timelines with revenue cycle management to minimize cash flow disruption and ensure claims can be submitted immediately upon enrollment approval.

Final Thoughts on Provider Enrollment and Credentialing: Get It Right From the Start

Provider enrollment and credentialing isn’t glamorous, but it’s the foundation of your practice’s financial viability. Every day of delay costs you revenue. Every error extends your timeline. And every missed recredentialing deadline can terminate your network participation and devastate cash flow.

The providers who succeed are those who start early, stay organized, follow up relentlessly, and know when to bring in professional help. This isn’t a process where “good enough” works—precision and persistence are essential.

Whether you’re opening a new practice, adding providers to an existing group, expanding to new locations, or credentialing for telehealth, TrueCare RCM has the expertise to navigate the complexities efficiently.

Get your provider enrollment and credentialing handled by experts:

TrueCare RCM – Provider Enrollment and Credentialing Services

- Complete CAQH profile setup and maintenance

- Medicare PECOS and Medicaid enrollment nationwide

- Commercial payer credentialing (all major insurance companies)

- Multi-state and multi-location enrollment

- Specialty-specific credentialing for all healthcare providers

- Recredentialing and compliance monitoring

- Full integration with medical billing services

Serving healthcare providers nationwide in: California | Texas | Florida | New York | Illinois | Michigan | Georgia | Maryland | Virginia | North Carolina | Arizona | Minnesota

Contact TrueCare RCM today:

- Phone: (323) 538-6467

- Email: info@truecarercm.com

Don’t let credentialing delays cost you another month of revenue. Schedule your free consultation and timeline assessment today.